Gold: Insurance for Prudent Investors

Precious metals reduce risk & preserve wealth

Responsible homeowners and landlords insure their property against fires, floods and violent storms. Sensible motorists insure their vehicles against inadvertent fender benders and costly collisions. Prudent investors own precious metals to protect financial assets from currency debasement, stock market meltdowns and economic collapse.

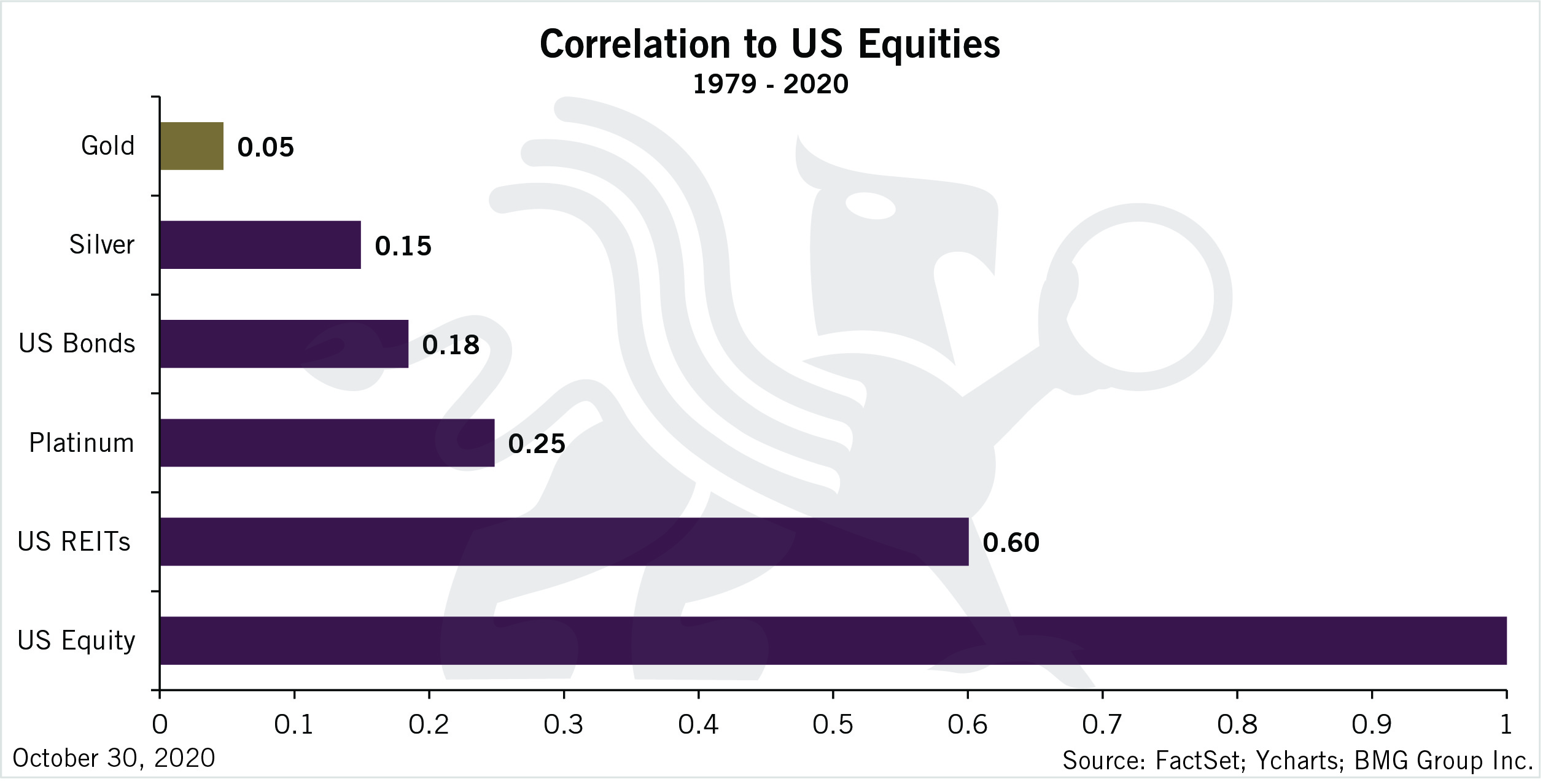

Reducing risk and avoiding financial loss is the purpose of insurance. Precious metals is the insurance plan that everyone needs – especially now. Like insurance, precious metals safeguard financial assets, reducing risk and loss. This is because gold is the most negatively correlated asset to financial assets.

They also offer peace of mind and preserve wealth during financial storms, unchecked debt expansion, and unforeseen political and geopolitical events – similar to what we are facing today.

Most people view gold, silver and platinum as commodities, and speculators trade the metals for short-term profit. Savvy savers, on the other hand, own bullion bars and coins as a long-term financial safe haven because they regard gold and silver as money and the foundation of the monetary system for thousands of years.

When assessing risk, each homeowner, auto owner and precious metal owner must determine if they’re adequately insured to protect their property, possessions and financial assets. The amount of coverage required depends upon one’s short- and long-term investment objectives, financial circumstances and comfort level.

Most home and business owners insure the contents of their property as well as the structure. Some auto owners carry only liability insurance on older models, while others prefer full coverage, especially on rare collector cars or newer vehicles with outstanding loan balances.

As with homeowner’s and car insurance, individuals and institutions who acquire precious metals must decide how much bullion they need to secure their financial portfolios during periods of inflation, deflation, stagflation and hyperinflation. The greater the perceived risk or potential loss, the higher the proportion of bullion needed.

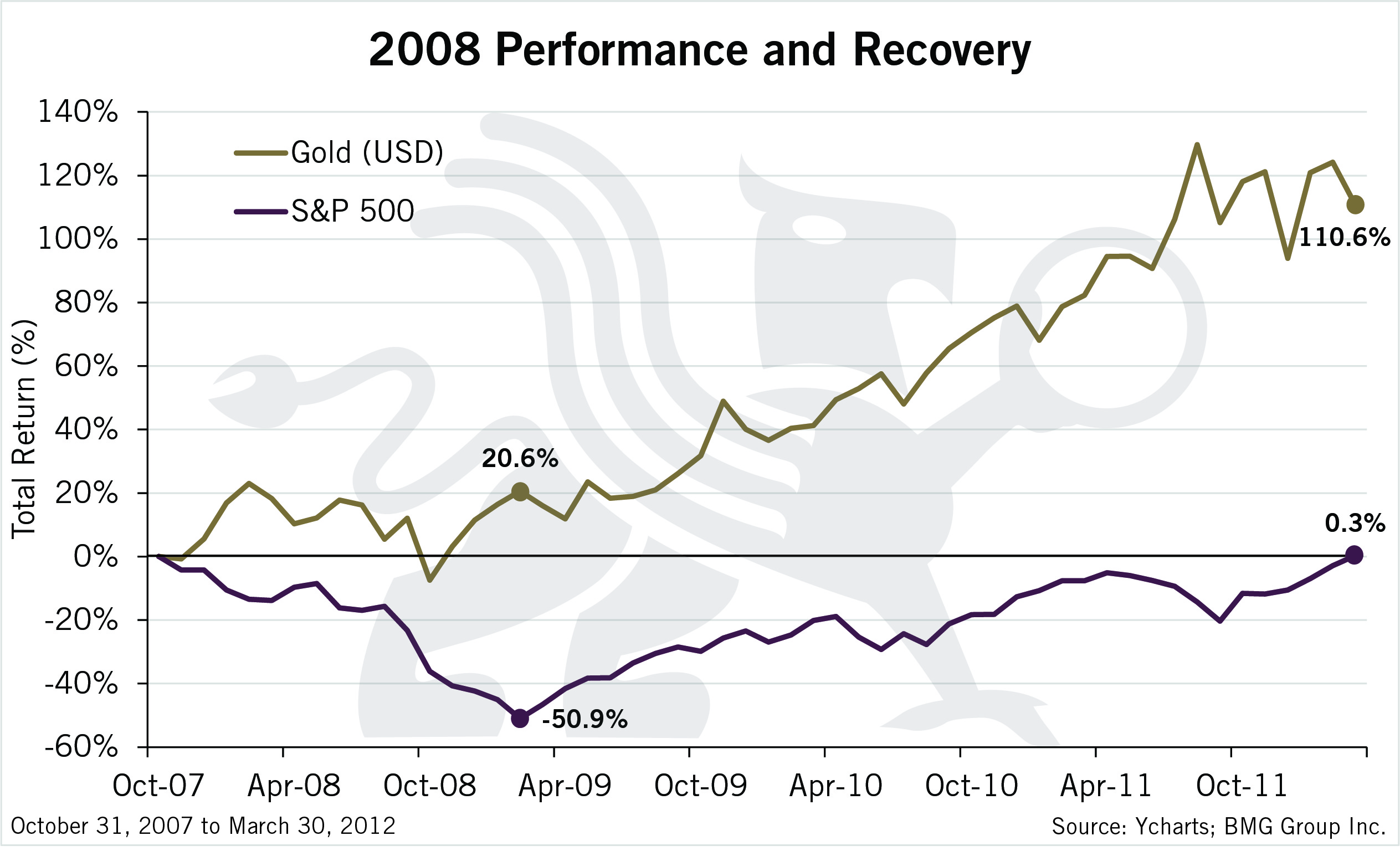

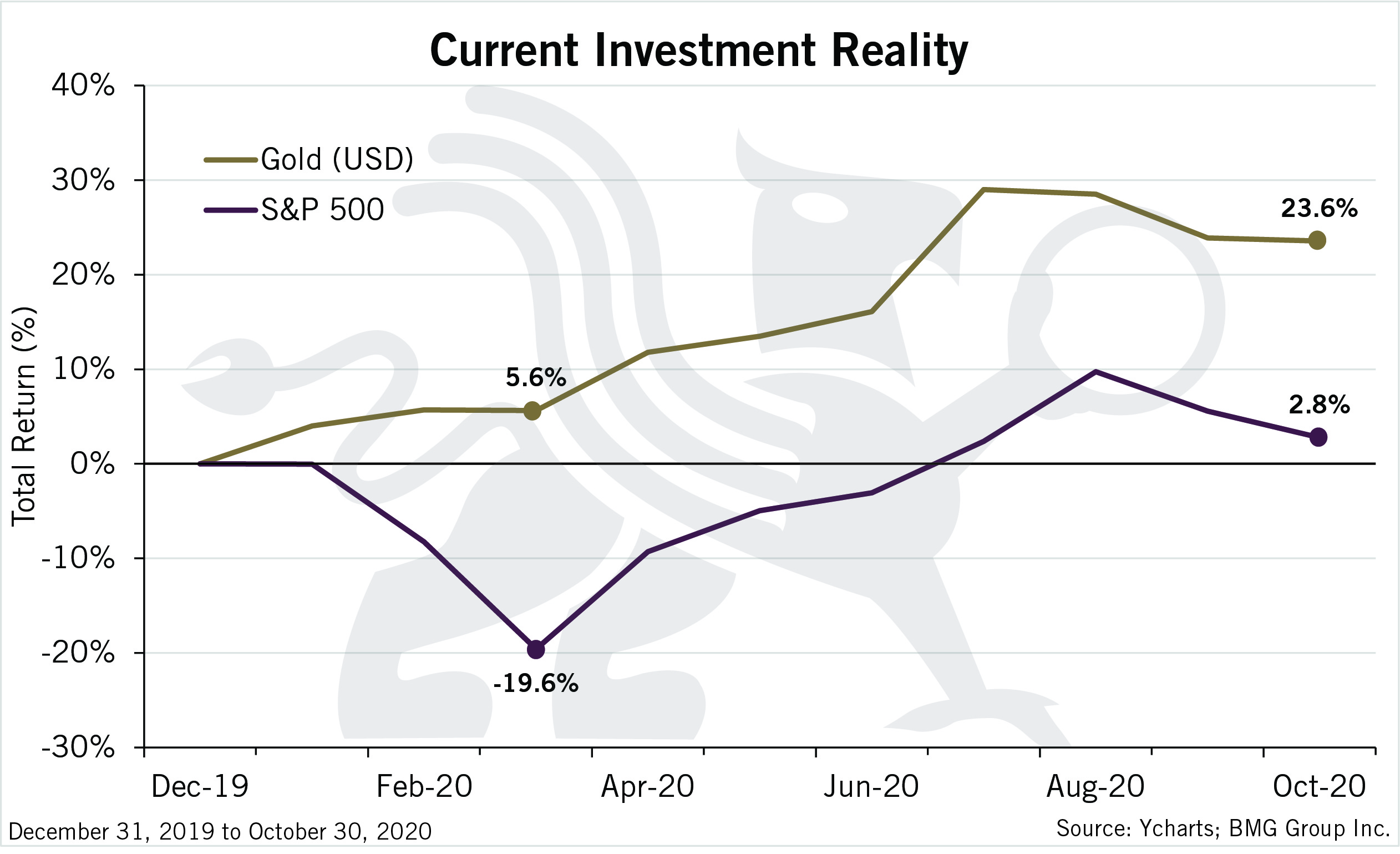

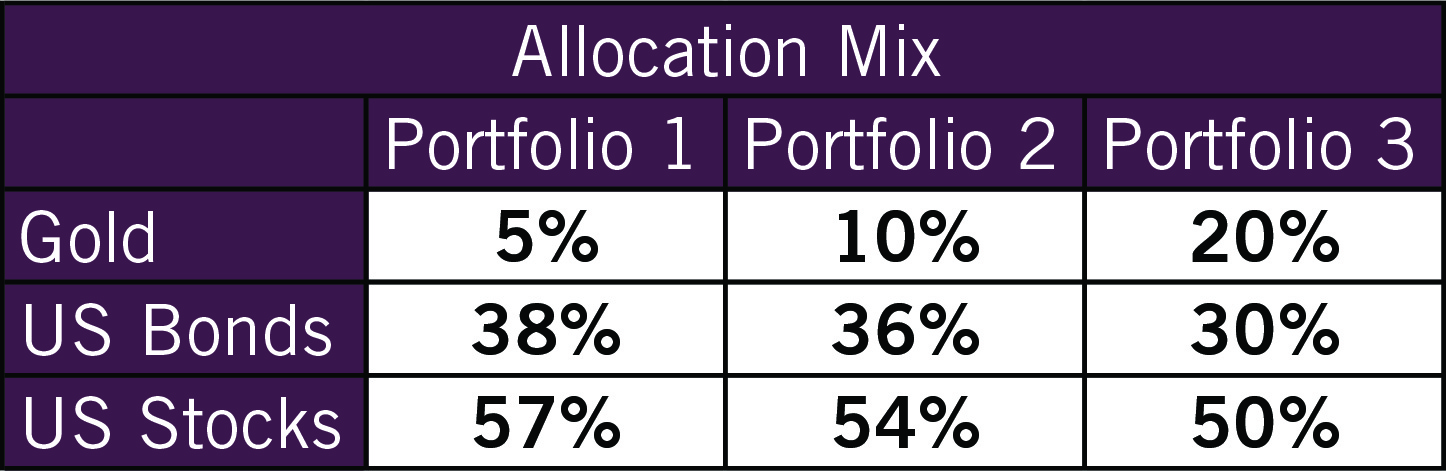

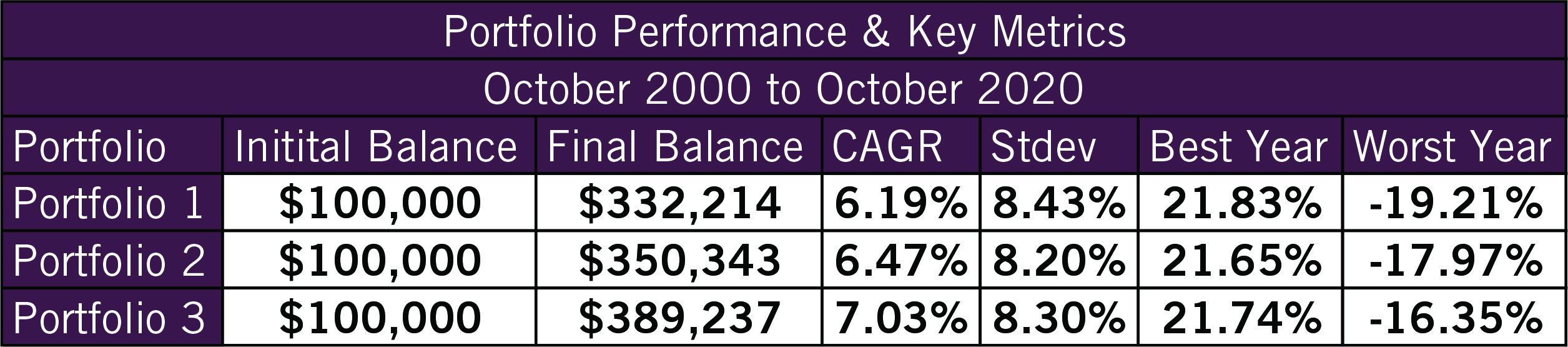

Some savers are satisfied holding 5 to 10 percent of their financial assets in physical gold and silver. Those who perceive a greater risk or loss—and desire a higher comfort and security level—prefer a higher percentage, ranging from 10 to 20 percent. Below is a comparative performance table based on holding 5, 10 and 20 percent in gold since 2000.

For those who buy and hold precious metals as insurance against currency debasement and financial calamity, it’s imperative to ensure your bullion is protected against theft and loss. Here are some factors to consider when deciding how and where to store your gold and silver stockpile:

- Banks don’t insure precious metals stored in personal safe deposit boxes and customers have no proof of what is in the safety deposit box.

- Exchange-Traded Funds (ETFs) that track gold, silver and platinum prices don’t insure unallocated metal holdings.

- Home insurance policies don’t cover bullion without a rider and additional premiums. Insurance on bullion stored at your home, if you can get it, is far more expensive than fees charged for allocated custodial storage.

Self-storage can also expose the owner to theft and home invasion. That’s why storing insured precious metals on an allocated basis in an LBMA member-vault is preferable. To protect the bullion owner, allocated custodial agreements must specify insurance and storage fees as well as the refiner, serial number, exact weight, and purity for each bar. The ownership details are necessary to validate which bullion bars belong to which investors. It will also provide proof of ownership should the custodian declare bankruptcy. It also attests the bullion is the property of the owner, not the custodian. If you’re not paying reasonable fees for insured storage, you probably don’t legally own the bullion.

As a result, the expenses of BMG’s mutual funds are slightly higher than a typical mutual fund that only holds paper assets. BMG’s custodian maintains insurance for all risks except for war, nuclear incident or government confiscation.

The best insurance is the kind you hope you never need to use. If that’s the case, bullion can provide peace of mind and wealth preservation for posterity. Like life insurance, precious metals can offer benefits to your family members and descendants for generations to come.

The information contained in this article provides a general overview of subjects covered, and the expressed personal views and opinions are not intended to be taken as advice regarding any product, organization or individual, and should not be relied upon as such. Consult your investment and legal advisors regarding specific coverage issues. Information and opinions expressed in this article are provided without warranty of any kind, either express or implied, including, without limitation, warranties of merchantability, fitness for a particular purpose, and non-infringement. BMG uses reasonable efforts to include accurate and up-to-date information from public domains and sources but does not make any warranties or representations as to its accuracy or completeness. BMG assumes no liability or responsibility for any errors or omissions in the content of this article.

Pingback: Gold Is the BEST Way To Reduce Portfolio Risk & Loss - Here's Why - munKNEE.com