How Pension Funds Can Secure Retirement Benefits After COVID | Nick Barisheff

Written for the Benefits and Pensions Monitor

In September 2019, I wrote an article, ‘Increased Pension Liabilities During the Coming Market Crash,’ which discussed current pension deficits and concluded that they were going to get much worse. At the time, no one anticipated the effect that COVID-19 would have on financial assets and gold.

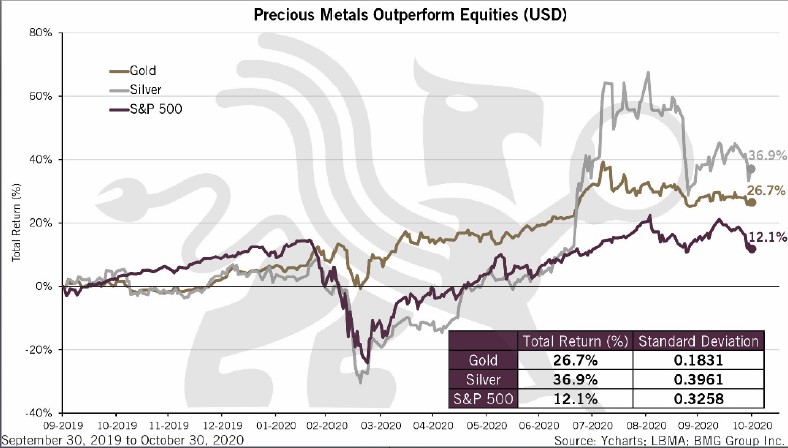

Since then, stocks have declined by 24 per cent and subsequently rebounded, while gold increased 27 per cent and silver 37 per cent (See Chart 1).

More importantly, while equity markets have recovered, the economy will not for years and the effect of lockdowns is still playing out. The Canadian Federation of Independent Business (CFIB) forecasts that Canada could experience 225,000 permanent business closures due to the pandemic1. So far, 5.3 million2 people have lost their jobs in the U.S., and 674,0003 in Canada. In 2021, bankruptcies will increase and more jobs will be lost. This will happen even if a vaccine becomes available. (See Chart 2)

Forced To Default

Commercial real estate – particularly hotels, retail, and office space – is another problem. As tenants are unable to pay rent and hotels have operated at less than 10 per cent occupancy due to lockdowns, landlords will be forced to default on their mortgages.

Office buildings will see a major reduction in future demand as many employees continue working from home. Residential real estate will be a problem as many tenants have not paid rent for months and have been protected from eviction (the eviction moratorium expires in December 20204). That will cause a ripple effect and result in a much bigger problem for the banks than the subprime mortgage crisis of 2008.

Even with a COVID-19 vaccine developed, many sectors of the economy will not return to normal. The travel industry, airline industry, hospitality industry, and many others will take years to return to pre-COVID activity.

All this will affect tax revenues. Municipalities will be hard hit since they depend on property taxes as their main source of revenue.

Earlier Losses

While the stock market has regained some of its earlier losses, all indexes are at extremely overvalued levels; a major correction is overdue.

All this does not bode well for pension funds, particularly those that have large unfunded liabilities. Interest rates and bond yields are unlikely to rise and equity returns are likely to decline sharply. Many REITs and major real estate projects will decline as income from tenants declines. Regional mall REITs have declined 54 per cent in 2020; lodging and resort REITs have declined 49 per cent; and office REITs have declined 30.2 per cent. In Canada, the Dundee Dream Office REIT, which holds $12 billion of prime office buildings, has declined 41 per cent.

Most pension fund managers and investment professionals use asset allocation to achieve diversification in order to reduce risk and maximize performance, thus responsibly managing their clients’ funds. The traditional view of portfolio management is to break portfolios into three asset classes (usually stocks, bonds, and cash) to achieve diversification.

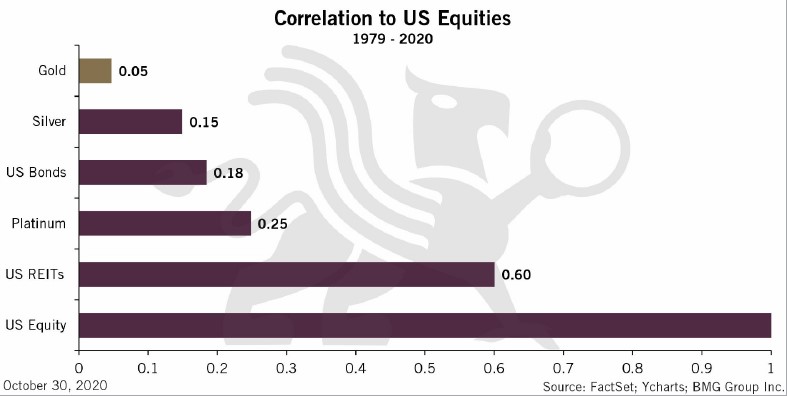

The definition of diversification maintains that a balanced investment portfolio should have various weightings of asset classes to be properly balanced. Furthermore, modern portfolio theory says that having the right mix of uncorrelated assets reduces risk and improves return. If that is the accepted practice, then why has the most negatively correlated asset group to stocks and bonds –precious metals bullion – been largely excluded from portfolio diversification?

Traditional View

The traditional view is simply incorrect and it has cost investors and pensioners dearly over the last decade alone.

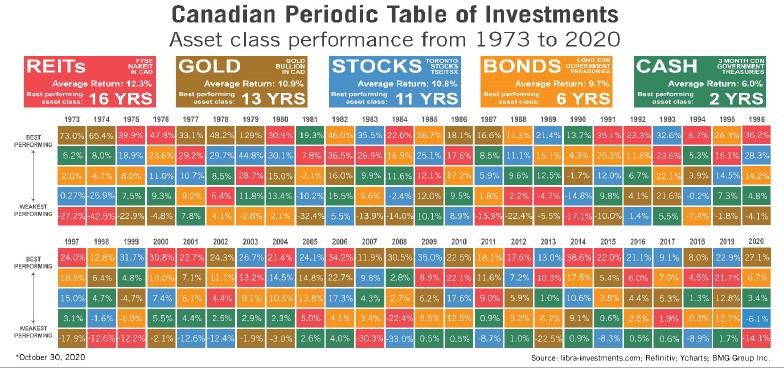

Pension fund returns have averaged 4.46 per cent over the past 10 years, while most pension funds need over six per cent to maintain their funding levels. Over the past 20 years, REITs have generally been the best-performing asset class, followed by gold, equities, bonds, and cash (See Table 1).

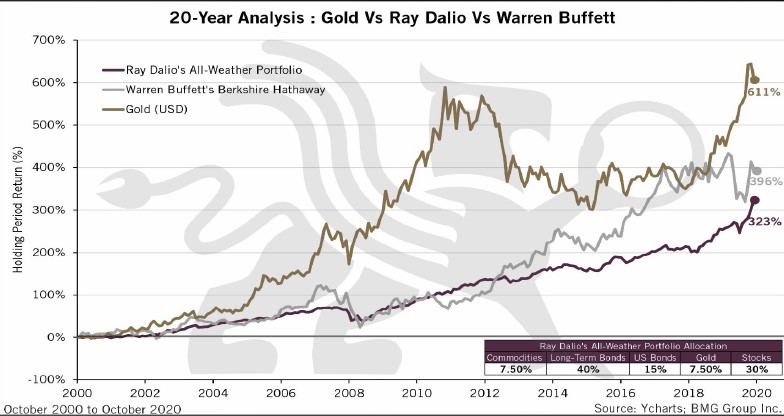

While pension funds were lucky to generate 4.6 per cent in annual returns, gold has averaged 10.4 per cent in U.S. dollars (USD) and 9.5 per cent in Canadian dollars (CAD) over the past 20 years. In 2019, it generated 18.8 per cent in USD and 12.9 per cent CAD. In 2020, the returns are even greater, with 23.6 per cent in USD and 27.1 per cent CAD. Gold outperformed both the Berkshire Hathaway and Ray Dalio’s All-Weather portfolio (See Chart 3).

Because gold is negatively correlated to financial assets, including gold in a portfolio would have improved returns while lowering portfolio volatility.

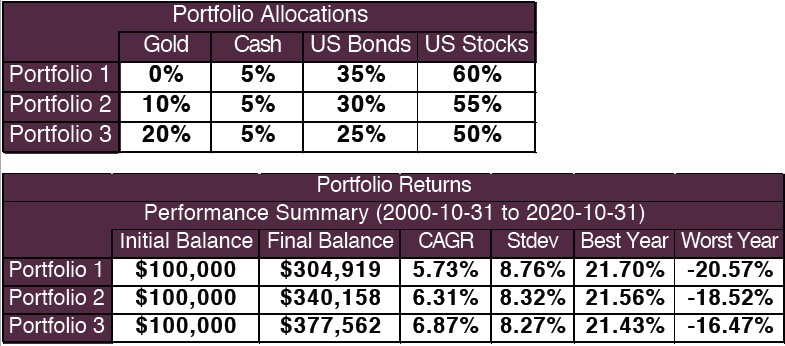

Since most pension funds and managed portfolios only hold a 60/40 allocation to stocks and bonds, the portfolio calculator developed by the World Gold Council 5 demonstrates the difference that a 10 per cent and 20 per cent allocation to gold would make in a portfolio (See Table 2).

However, there are few pension funds that have an allocation to gold. In September 2020, the Ohio Police and Fire Pension Fund announced it will allocate five per cent of its assets to gold. With $15.7 billion in assets under management, a five per cent allocation equates to over $750 million (See Chart 4).

Some pension funds have already defaulted on promises made to beneficiaries and class action lawsuits have begun. These will surely increase in time and portfolio managers will be held accountable.

There is about $33 trillion invested in pension funds6, so 10 per cent would equal $3.3 trillion of gold. Considering that annual mine supply is about $200 billion, only a few early adopters will be able to obtain a proper gold allocation in the future. Gold production remains relatively flat at 3,500 tonnes, while demand has increased to 4,800 tonnes over the past few years.

To acquire even a five per cent allocation, many pension funds will need to acquire billions in gold. Any pension fund slow to start a progressive gold acquisition program will be left out or forced to pay much higher prices as more pension funds decide they must allocate to gold. While paper proxies may be available, they defeat the fundamental reason for owning gold, no counter-party risk.

- https://www.cfib-fcei.ca/en/media/news-releases/cfib-statement-manysmall-

businesses-far-too-fragile-survive-another-round - https://www.bls.gov/web/empsit/cpseea01.pdf

- https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1410028703

- https://www.federalregister.gov/documents/2020/09/04/2020-19654/

temporary-halt-in-residential-evictions-to-prevent-the-further-spreadof-

covid-19 - https://www.gold.org/goldhub/portfolio-tools/simulator?utm_

source=google&utm_medium=cpc&utm_campaign=rwmgoldhub&

utm_content=470087778228&utm_term=gold per cent20de

mand&gclid=EAIaIQobChMIzKHbxqH77AIVRL7ACh0zMAwrEAAYASACEgJt

m_D_BwE - https://www.oecd.org/pensions/Pension-Funds-in-Figures-2020.pdf